RHODE ISLAND HOMEOWNERS

COVID-19 RESOURCES

We understand that these are stressful times for homeowners who may be experiencing loss of income and other financial impacts related to the COVID-19 health crisis. RIHousing is working hard to ensure that Rhode Island homeowners have the resources and information they need. Visit our general COVID-19 information here.

CARES Act Mortgage Forbearance:

What You Need to Know

HELPFUL RESOURCES

- Mortgage and Housing Assistance during COVID-19

Consumer Financial Protection Bureau - Guide to mortgage relief options

Consumer Finance Protection Bureau - HomesRI Homeowner FAQs

- HomesRI Hoja Informativa para los Dueños de Casa

- HomesRI Utility Fact Sheet (ENG/SP)

- Assistance in Making Your Mortgage Payments

FORECLOSURES

- Extension of Foreclosure and Eviction Moratorium: Single-family Homeowners w/FHA-insured Mortgages

Updated June 24, 2021

BEWARE OF SCAMS

- Beware of scams related to the coronavirus

Consumer Finance Protection Bureau - COVID-19 Consumer Warnings and Safety Tips

Federal Communications Commission

For homeowners who have not experienced a loss of income and are able to make their mortgage payments, it is important that you continue to do so. However, many homeowners may be facing hardships that make that impossible. The first step for homeowners struggling to make their mortgage payments should be to reach out to their mortgage servicer to discuss available options.

UPDATED 05/12/2021

Deadline for Government insured (FHA, VA, USDA) Mortgage Forbearance Requests

If you have a government insured mortgage (FHA, VA, USDA) and you are experiencing a financial hardship that negatively impacts your ability to make on-time mortgage payments due to the COVID-19 National Emergency and would like to request a mortgage forbearance, please be aware that the forbearance ends on September 30, 2022. After September 30, 2022, you may still be eligible for other FHA loss mitigation options. These options will require you to provide written documentation of your hardship.

If you have a FNMA loan, you may be eligible to extend your forbearance for up to two additional 90-day periods once you have reached the completion of your 12-month forbearance.

If you are a RIHousing mortgage customer and you are interested in applying for a mortgage forbearance due to a COVID-19 related hardship, please submit your request to servicinginfo@rihousing.com. In your request you must affirm that you are suffering a financial hardship due to the COVID-19 National Emergency. If you are unsure what type of mortgage you have, please contact RIHousing at 401-457-1180 or 1-800-854-1180.

Things to ask your mortgage servicer:

Ask your mortgage servicer how you will be required to pay back the amount owed after the forbearance period ends. You may have the option to:

- Pay back the amount owed in one lump sum

- Extend the term of your mortgage loan so that deferred payments are added at the end of your mortgage

- Make higher monthly payments for a period of time to pay back the deferred amount

CARES Act

A new federal law, the Coronavirus Aid, Relief, and Economic Security (CARES) Act, puts in place protections for homeowners with federally backed mortgages:

- A right to forbearance for homeowners who are experiencing a financial hardship due to the COVID-19 emergency.

If you don’t have a federally backed mortgage, you still may have relief options through your mortgage servicer or from your state.

When to contact the RIHousing HelpCenter:

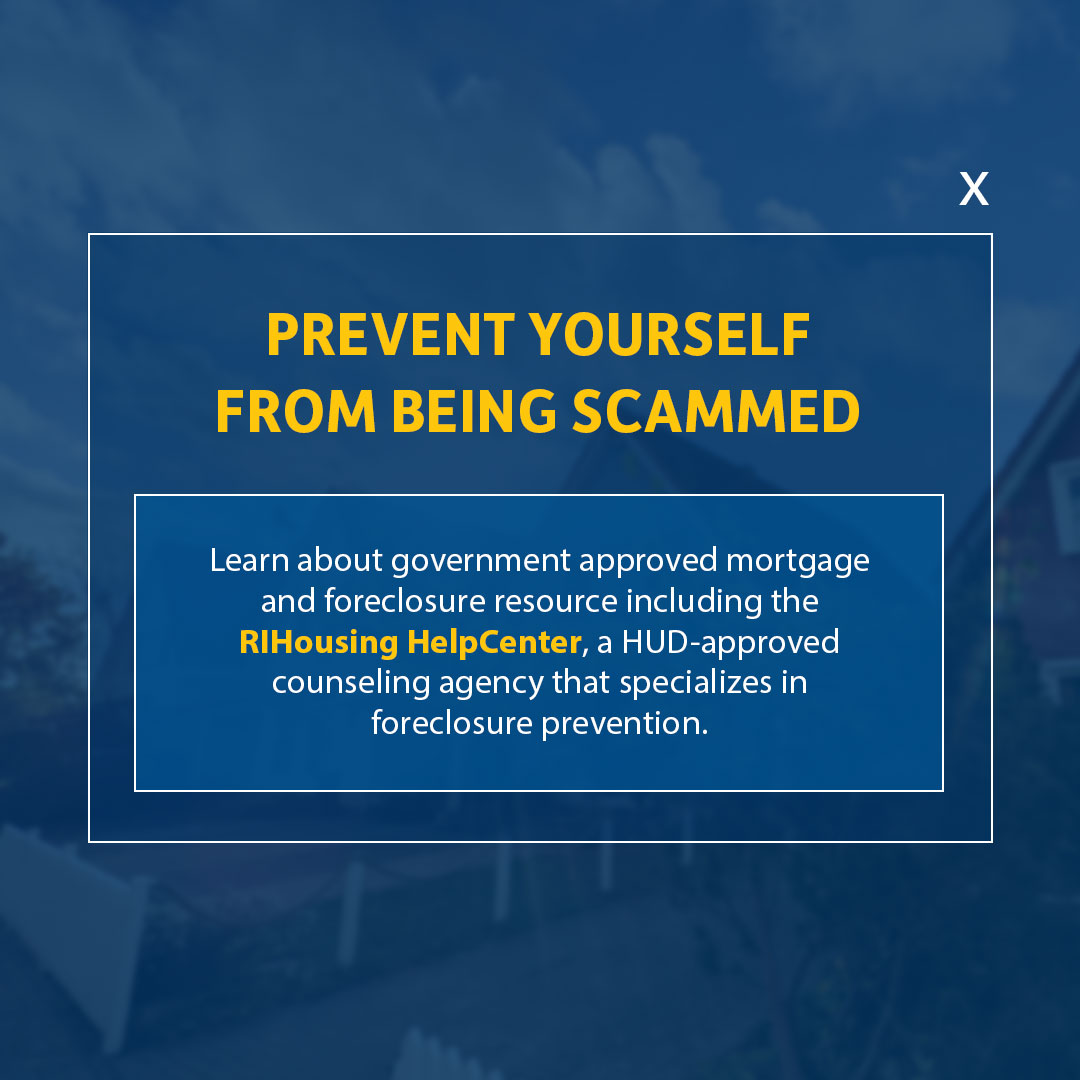

RIHousing’s HelpCenter is a HUD-approved counseling agency that provides free foreclosure prevention counseling services to all Rhode Island homeowners.

If you have already contacted your mortgage servicer but have been denied a forbearance for your mortgage, contact the HelpCenter.

To get started, complete and submit the Financial Information Package.

If you need assistance with completing the Financial Information Package, please contact the HelpCenter at 401-457-1130.

MEDIATION

RIHousing provides mediation services pursuant to RI General Laws §34-27-3.2 and 230-RICR-40-10-4. The Mortgage Foreclosure and Sale Act gives homeowners who are delinquent on their mortgage the right to a mediation conference with their mortgage lenders to facilitate a resolution to avoid foreclosure. This service is free of charge to homeowners.

If you have received a mediation notice from your lender and wish to take advantage of the mediation process, please reach out. While we are no longer holding in-person meetings, staff are available via email and/or telephone as needed. Mediation conferences and foreclosure counseling are now held via phone.

Contact:

Mediation Coordinator

mediationcoordinator@rihousing.com

401-457-1213

Beware of scammers who offer you mortgage loan relief or promise to save your home. Watch for signs of a scam and protect yourself.

Signs that may mean you are getting scammed

Watch out for the following signs as they may mean you are being scammed:

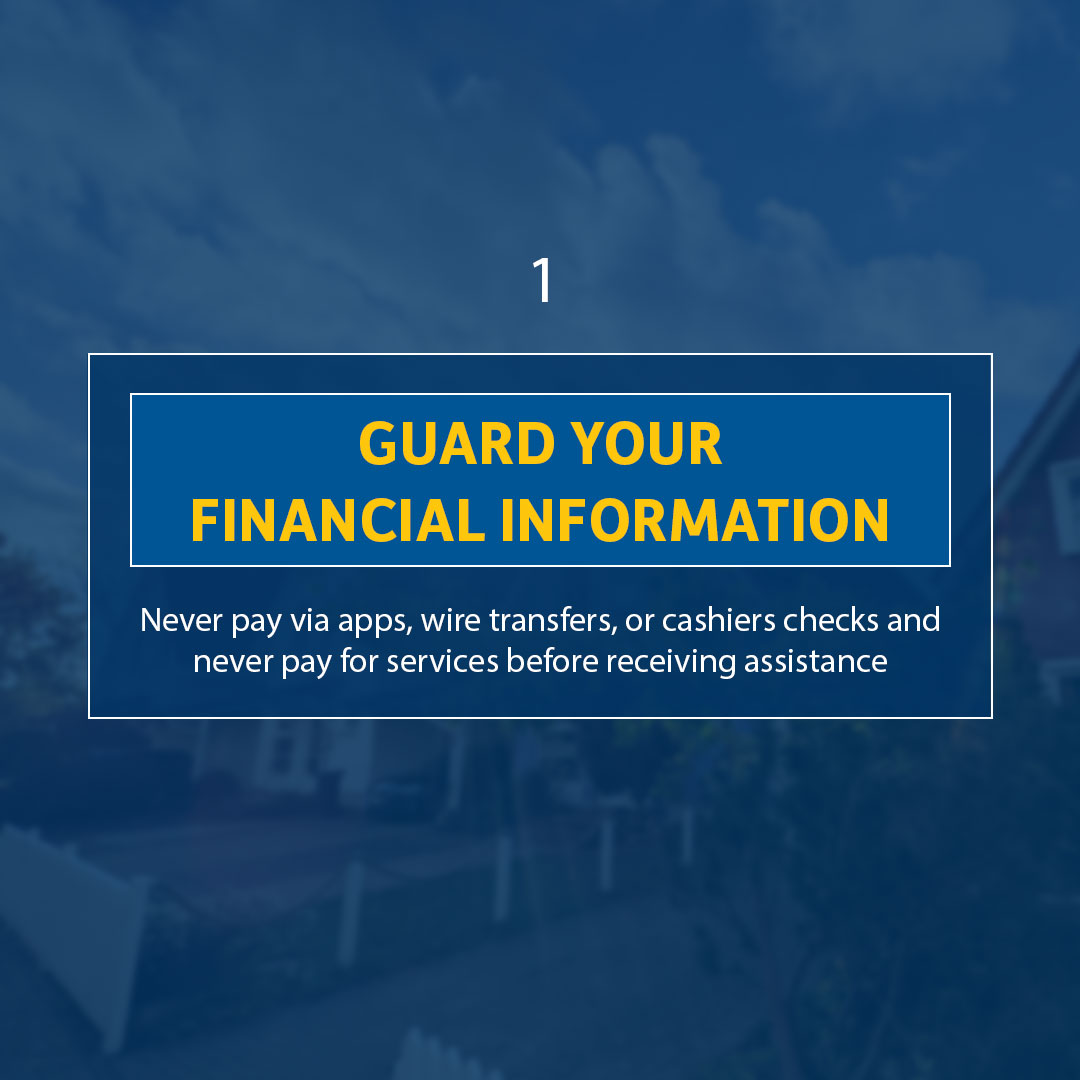

- They ask you to wire money, pay by cashier’s check, use an app for payment, or ask for your credit card information before you receive assistance.

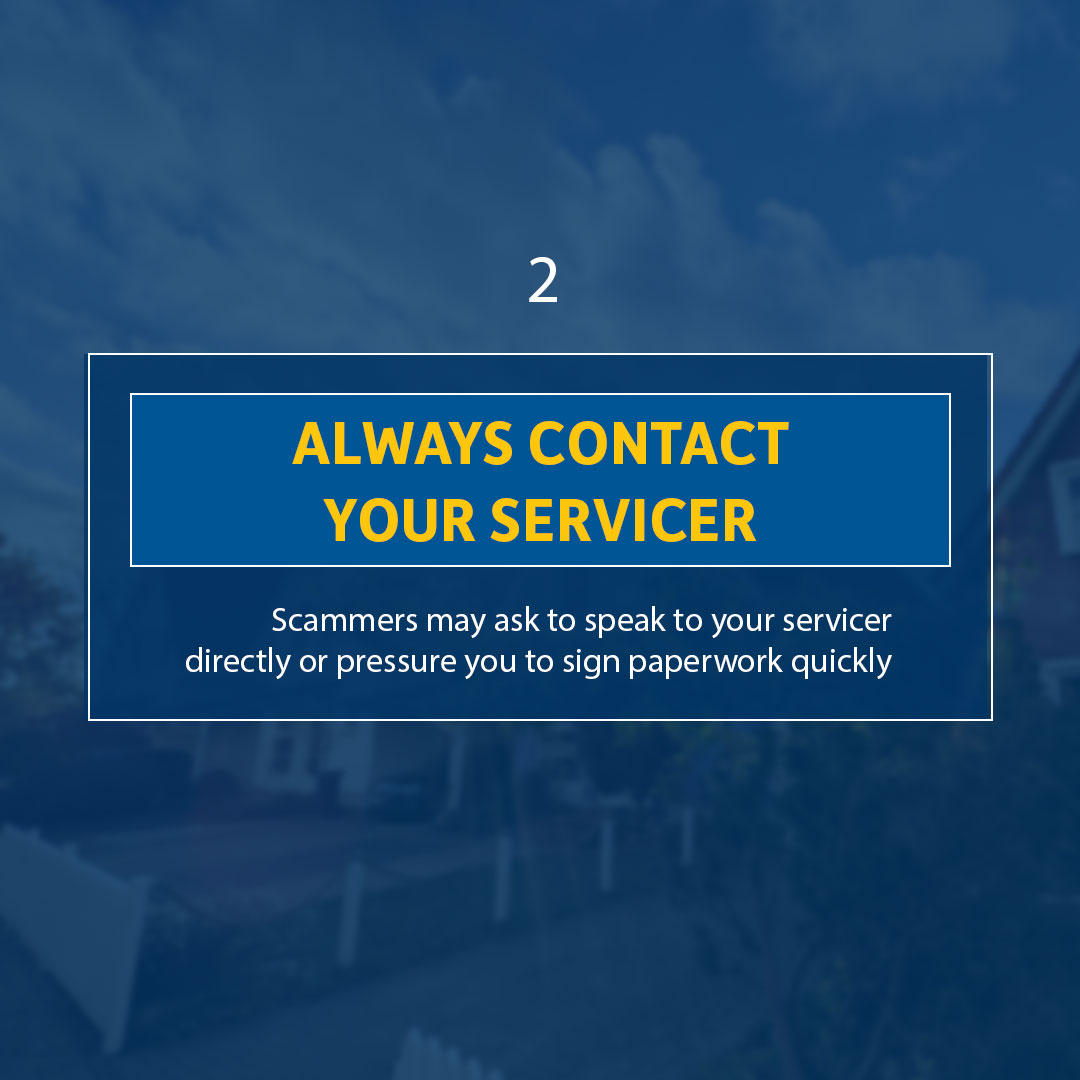

- They ask you to stop speaking with or offer to speak directly to your lender.

- They pressure you to sign paperwork without enough time to review documents carefully.

- They ask you to sign the deed to your home to them or offer to rent your home to you.

- They offer special programs or assistance to prevent foreclosure.

Ways to protect yourself

- DO NOT share your credit card information right away.

- DO NOT wire money or send money using an app.

- DO NOT sign paperwork or other documents you have not been able to review.

- DO NOT send mortgage payments to companies that are not your loan servicer.

- DO speak with your loan servicer if you are having trouble paying your mortgage.

- DO learn about government approved mortgage and foreclosure resources, including the RIHousing HelpCenter, a HUD-approved counseling agency that specializes in foreclosure prevention.

- DO report mortgage relief scams if you suspect you’ve encountered one.

If you believe you have been a victim of fraud, report it to:

- The Federal Trade Commission (FTC)

- Your state attorney general: consumers@riag.ri.gov

Educate yourself on mortgage relief scams, your rights as a homeowner, how to get help and what to do if you’ve been scammed. The Federal Trade Commission (FTC) has additional helpful information on mortgage relief scams online.

Frequently Asked Questions – Forbearance

What is a forbearance?

A forbearance is a temporary pause or reduction of mortgage payments for a specified period of time. This short-term payment relief provides customers with assistance right away.

Do customers need to repay the mortgage payments from the forbearance period?

Yes. Forbearance doesn’t erase what a customer owes; customers will need to repay any missed or reduced payments in the future.

Will a customer’s credit be affected if they receive a forbearance due to COVID-19?

A forbearance related to COVID-19 will not have a negative impact on a customer’s credit.

If a customer receives a forbearance due to COVID-19, here’s what they should know:

- If current on mortgage payments as of January 31, 2020, credit will not be affected by the forbearance – your lender should report the loan as current.

- If a customer was not current on mortgage payments as of January 31, 2020, the customer will still have credit protection from the forbearance. Your lender should not report payments that are paused during forbearance as late. However, payments that were reported as late prior to January 31 will still show up as “late” on the customer’s credit report.

Does everyone that applies receive a forbearance?

The CARES Act protects borrowers with federally backed mortgages who became delinquent after 2/1/2020 due to a COVID-relates hardship resulting in a loss of income. Only mortgage holders who meet these criteria are eligible for a mortgage forbearance.

Although only homeowners with federally-backed mortgages are covered under the CARES Act, some lenders are making the choice to provide relief to homeowners that are not covered.

Homeowners should contact their mortgage servicer to find out if other help is available.

What should customers who are still working but with reduced work hours do if unable to make their full mortgage payment?

Customers have the option of receiving a mortgage forbearance while continuing to pay whatever amount they can during the forbearance period. This will make the amount owed at the end of forbearance more manageable.

Your mortgage servicer can discuss this option more fully.

Frequently Asked Questions – Post-Forbearance

What happens after the forbearance period ends?

Unless a customer receives further relief, once the forbearance period ends, they will need to resume their regular mortgage payment schedule and repay any missed or reduced payments from the forbearance period.

At the end of the forbearance period, what options are there for customers to pay the past due amount?

There are several options to pay the past due amount:

- For those that can afford to, the simplest thing to do is make a lump sum payment and pay off the amount owed from the forbearance.

- Apply for a repayment plan. If approved, the customer will pay a portion of the past due amount each month in addition to the regular mortgage payment.

- Apply for a loan modification. By modifying the loan, the balance from the forbearance period is added back into the mortgage.

Mortgage customers should discuss these options with their servicer to better understand available options.