RIHOUSING MORTGAGE CUSTOMERS

COVID-19 Resources

Check our COVID-19 Information page for updates and information.

Homeowner but not a RIHousing mortgage customer? Visit our Rhode Island Homeowners COVID-19 page.

UPDATED 05/12/2022

Deadline for government insured (FHA, VA, USDA) Mortgage Forbearance Requests

If you have an government issued mortgage (FHA, VA, USDA) and you are experiencing a financial hardship that negatively impacts your ability to make on-time mortgage payments due to the COVID-19 National Emergency and would like to request a mortgage forbearance, please be aware that the forebearance ends on September 30, 2022. After September 30, 2022, you may still be eligible for other FHA loss mitigation options. These options will require you to provide written documentation of your hardship.

If you are a RIHousing mortgage customer and you are interested in applying for a mortgage forbearance due to a COVID-19 related hardship, please submit your request to servicinginfo@rihousing.com. In your request you must affirm that you are suffering a financial hardship due to the COVID-19 National Emergency. If you are unsure of what type of mortgage you have, please contact RIHousing at 401-457-1180 or 1-800-854-1180.

Beware of scammers who offer you mortgage loan relief or promise to save your home. Watch for signs of a scam and protect yourself.

Signs that may mean you are getting scammed

Watch out for the following signs as they may mean you are being scammed:

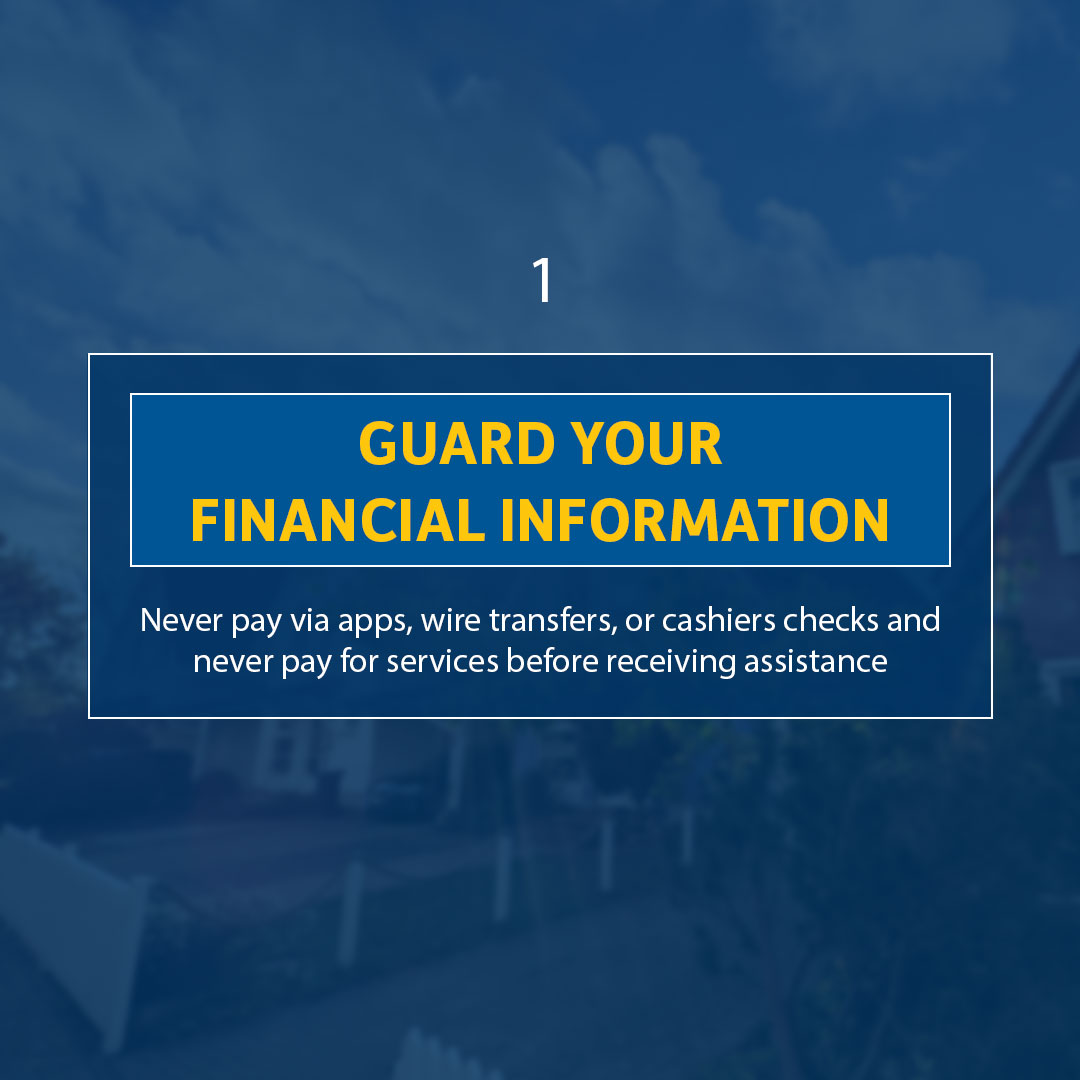

- They ask you to wire money, pay by cashier’s check, use an app for payment, or ask for your credit card information before you receive assistance.

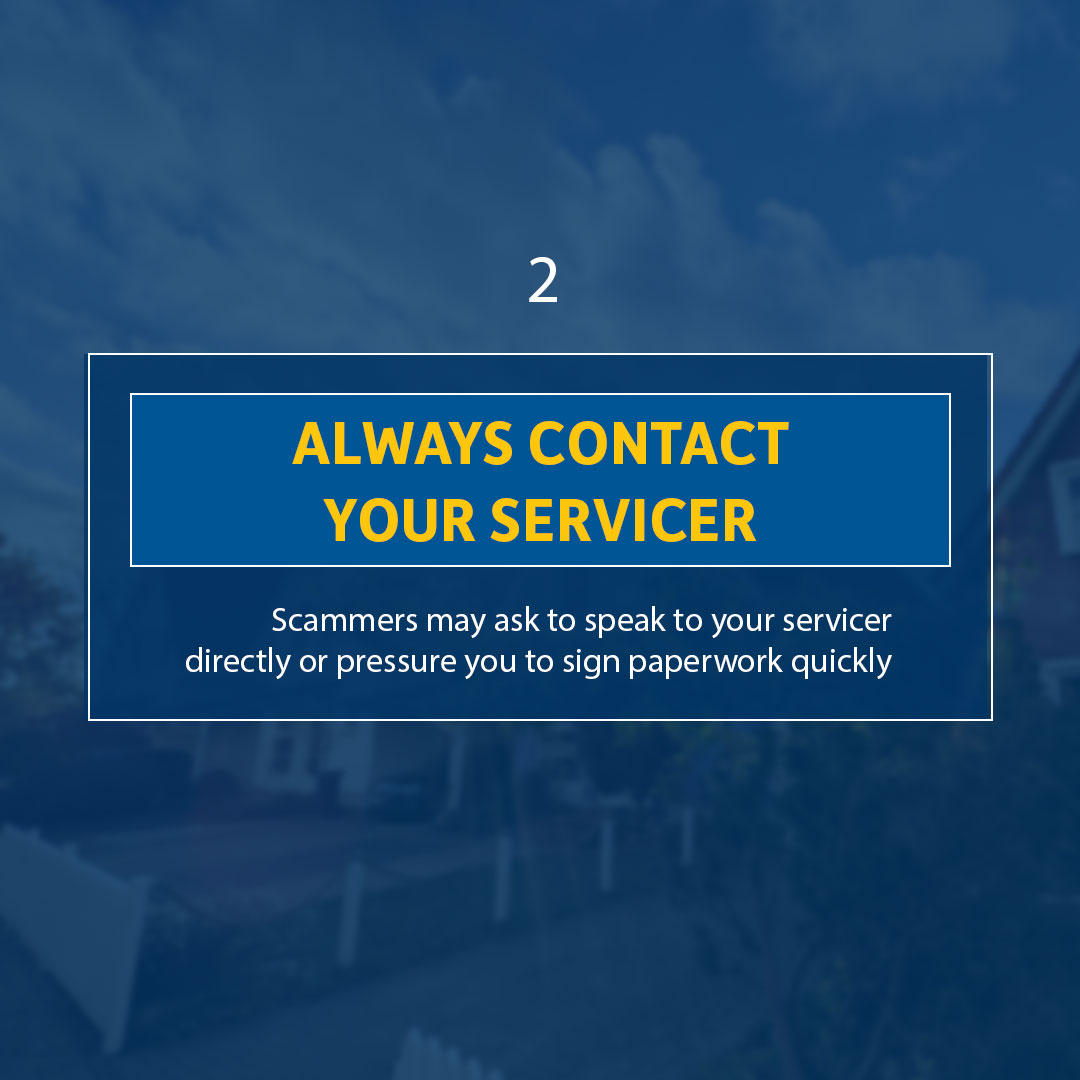

- They ask you to stop speaking with or offer to speak directly to your lender.

- They pressure you to sign paperwork without enough time to review documents carefully.

- They ask you to sign the deed to your home to them or offer to rent your home to you.

- They offer special programs or assistance to prevent foreclosure.

Ways to protect yourself

- DO NOT share your credit card information right away.

- DO NOT wire money or send money using an app.

- DO NOT sign paperwork or other documents you have not been able to review.

- DO NOT send mortgage payments to companies that are not your loan servicer.

- DO speak with your loan servicer if you are having trouble paying your mortgage.

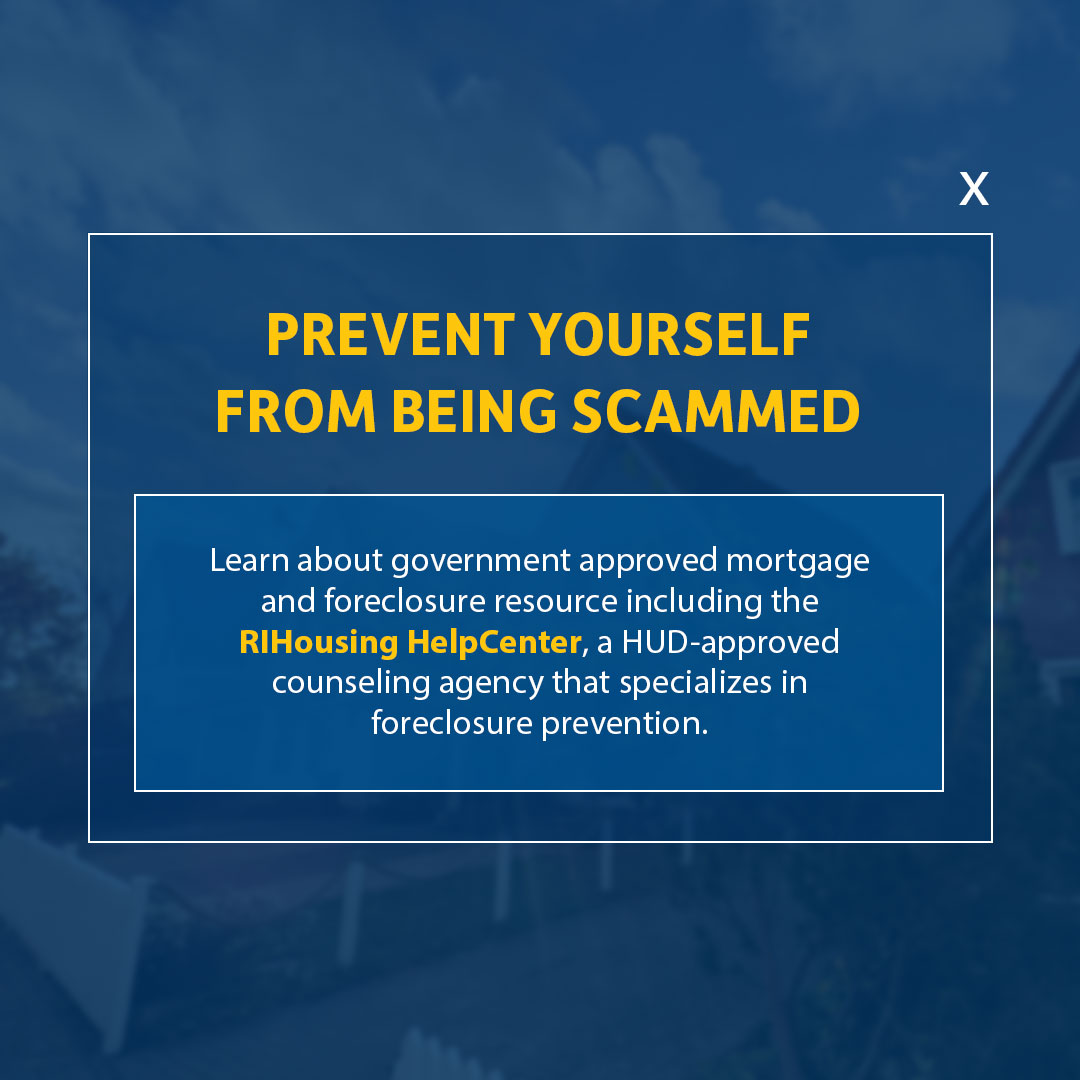

- DO learn about government approved mortgage and foreclosure resources, including the RIHousing HelpCenter, a HUD-approved counseling agency that specializes in foreclosure prevention.

- DO report mortgage relief scams if you suspect you’ve encountered one.

If you believe you have been a victim of fraud, report it to:

- The Federal Trade Commission (FTC)

- Your state attorney general: consumers@riag.ri.gov

Educate yourself on mortgage relief scams, your rights as a homeowner, how to get help and what to do if you’ve been scammed. The Federal Trade Commission (FTC) has additional helpful information on mortgage relief scams online.

Frequently Asked Questions

Last Updated: April 15th, 2020

Loan Forbearance

What should RIHousing mortgage customers do if they can’t make their mortgage payment due to losing their job during the COVID-19 health crisis?

Mortgage customers who are experiencing reduced hours or job loss and are having difficulty making their mortgage payments should submit a forbearance request via email to servicinginfo@rihousing.com. Requests must provide a description of the hardship.

What should customers do who are working but concerned over potentially losing their job due to cuts relating to the COVID-19 health crisis?

For those who are able to make their mortgage payments, it is important that they continue to do so.

If their situation changes and they are no longer able to make their payments, customers should reach out to review available options.

What mortgage assistance programs are available to RIHousing mortgage customers?

If COVID-19 has impacted a customer’s ability to make mortgage payments, he/she may qualify for a forbearance, which is a way to pause mortgage payments without damaging a customer’s credit.

The recently passed CARES Act (“Coronavirus Aid, Relief, and Economic Security” Act) mandates that all borrowers with government-backed mortgages be allowed to delay mortgage payments during a forbearance period.

What is a forbearance?

A forbearance is a temporary pause or reduction of mortgage payments for a specified period of time. This short-term payment relief provides customers with assistance right away. Once that timeframe is up, we will reevaluate a customer’s situation and determine the next step.

Do customers need to repay the mortgage payments from the forbearance period?

Yes. Forbearance doesn’t erase what a customer owes; customers will need to repay any missed or reduced payments in the future.

Why is RIHousing not offering payment forgiveness?

RIHousing services your mortgage for federal agencies such as Fannie Mae, Freddie Mac and Ginnie Mae and we are contractually obligated to follow their guidelines, which do not provide for payment forgiveness. However, each federal agency has a variety of loan modification programs designed to help you bring your account current. Rest assured that RIHousing will work with you to provide the best possible terms to bring your account current at the conclusion of your forbearance plan.

Will customers incur any additional fees during the mortgage forbearance?

No, RIHousing will not charge any late fees during the forbearance period.

Will a customer’s credit be affected if they receive a forbearance due to COVID-19?

A forbearance related to COVID-19 will not have a negative impact on a customer’s credit. If a customer receives a forbearance due to COVID-19, here’s what they should know:

- If current on mortgage payments as of January 31, 2020, credit will not be affected by the forbearance – we’ll report the loan as current.

- If a customer was not current on mortgage payments as of January 31, 2020, the customer will still have credit protection from the forbearance. We will not report payments that are paused during forbearance as late. However, payments that were reported as late prior to January 31 will still show up as “late” on the customer’s credit report.

Does everyone that applies receive a forbearance?

The CARES Act protects borrowers who became delinquent after 2/1/2020 due to a COVID-relates hardship resulting in a loss of income.

Only mortgage holders who meet these criteria are eligible for a mortgage forbearance.

What should customers who are still working but with reduced work hours do if unable to make their full mortgage payment?

Customers have the option of receiving a mortgage forbearance while continuing to pay whatever amount they can during the forbearance period. This will make the amount owed at the end of forbearance more manageable

What happens if a customer returns to work during the forbearance period?

It is important that customers notify us when they return to work so that we can review what options may be available. If income is restored, customers should reach out to RIHousing and resume making payments as soon as possible.

How do customers know if they have been approved for a forbearance on mortgage payments?

Once approved for a forbearance, we will send a letter to the customer outlining the dates of the forbearance period.

Post-Forbearance

What happens after the forbearance period ends?

Once the forbearance period ends, they will need to resume their regular mortgage payment schedule and repay any missed or reduced payments from the forbearance period.

At the end of the forbearance period, what options are there for customers to pay the past due amount?

There are several options to pay the past due amount:

- For those that can afford to, the simplest thing to do is make a lump sum payment and pay off the amount owed from the forbearance. We understand that this may not be possible, so other options include:

- Apply for a repayment plan. If approved, the customer will pay a portion of the past due amount each month in addition to the regular mortgage payment.

- Apply for a loan modification.

What happens at the end of the forbearance period if a customer still cannot make mortgage payments?

For those customers needing additional assistance at the end of the forbearance period, we will work with them to identify the available options. Options will depend on who the investor/insurer is for the mortgage.

If you are a RIHousing mortgage customer and need assistance during this time, please reach out.

- Please note that the current call volume is extremely high, so we ask for your patience and understanding while we do our best to assist all customers. You may also reach us at servicinginfo@rihousing.com.

- Mortgage customers who are experiencing reduced hours or job loss and are having difficulty making their mortgage payments should submit a forbearance request via email to servicinginfo@rihousing.com. Requests must provide a description of the hardship.

- If you have an FHA insured mortgage and need assistance making your mortgage payments, click here to learn more.